2011 has been another ride on the financial roller coaster. Anyone who has not felt the tremors, bumps and absolute death drops of the economy is extremely lucky. The same is true of small and large businesses alike, even though there are some rays of hope breaking through the cloudy economic storms. It’s arguable that the natural and organic industry is among the bright spots.

According to the 2011 WholeFoods Retailer Survey, many stores are reporting strong sales numbers, and are clearly thriving businesses in their communities as evidenced by heavy foot traffic and good spending per transaction. Other establishments may just be making ends meet, and are feeling the  sting of lost jobs in their areas (thereby fewer shoppers and less spending). Overall sales are down slightly, which is not surprising given the shape of our economy. The type of stores that took part in this year’s survey is another contributing factor: Compared with past years, most participants were from smaller stores with less revenue. Given the economy, expansion activity was muted this year.

sting of lost jobs in their areas (thereby fewer shoppers and less spending). Overall sales are down slightly, which is not surprising given the shape of our economy. The type of stores that took part in this year’s survey is another contributing factor: Compared with past years, most participants were from smaller stores with less revenue. Given the economy, expansion activity was muted this year.

But a truly reassuring sign of our industry’s strength and health is that net profits jumped, as did average net profits per square foot. For the 2011 Retail Universe breakdown of sales, see page 29. These and other figures that will be presented in this article are encouraging. We know times are tough, but independent stores are resilient and are committed to doing what they do best: offering their communities the knowledge and tools required to lead healthy lives. And, there’s no sign of them shrinking away from this task any time soon.

Our gratitude goes out to all the stores that took the time to participate in this year’s survey. Without your help, this analysis would not be possible. And congratulations to Health Hut, Brentwood, CA, which was randomly selected from all survey participants to receive a cash prize of $100. And, a special thank you to Jay Jacobowitz, president and founder of Retail Insights and WholeFoods Magazine merchandising editor, who played a key role in helping to interpr et this year’s survey data.

et this year’s survey data.

Smaller, But Mighty Retailers

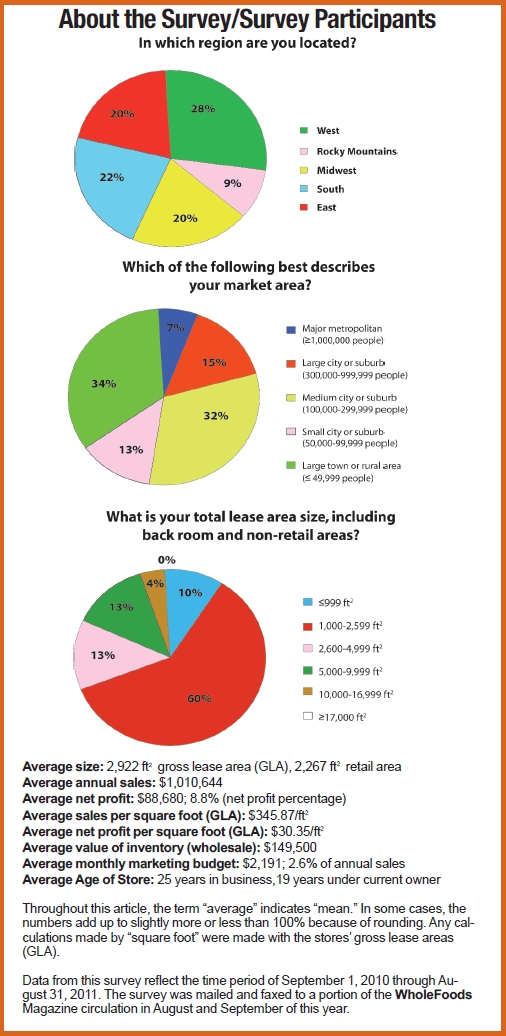

Let’s first talk about some characteristics of this year’s survey respondents before delving into the sales data. Stores represented all U.S. regions and population areas, though this year they were more heavily from medium cities and suburbs with populations of 100,000–299,999 people (32% in 2011 versus 22% in 2010). Both years had a strong representation of stores from large towns or rural areas with populations of less than 50,000 people (34% in 2011 and 40% in 2010).

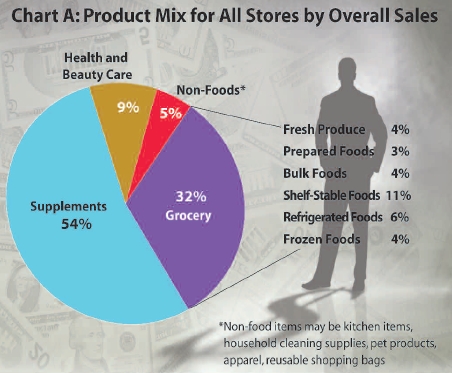

As in years past, establishments predominantly had brick and mortar stores and were heavy supplement sellers (see Chart A). Though about 27% do some form of online sales, just 2.4% of all revenue came from online sales.

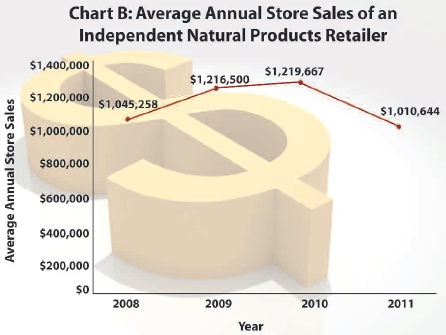

Compared with last year’s numbers, 2011 respondents were from clearly smaller stores with nearly 15% smaller gross lease areas (GLA) (2,922 ft2 in 2011 versus 3,424 ft2 in 2010). In fact, this year’s survey takers only averaged 2,269 ft2 of retail selling space. No large stores of 17,000+ ft2 participated this year. Therefore, it’s not a huge surprise that the 2011 bank of independent natural products stores (combined with a stagnant economy) resulted in a 17% decline in average store sales ($1,010,644 in 2011 versus $1,219,667 in 2010) (see Chart B).

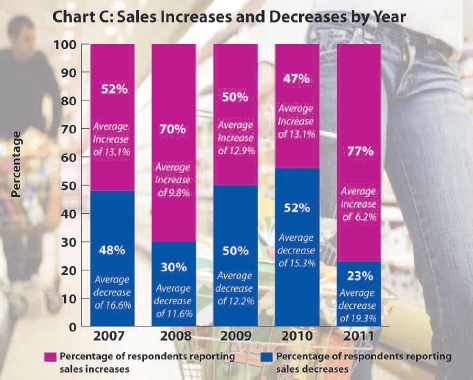

Now is a good time to add that stores were directly asked whether their sales increased or decreased over the past year. An overwhelming majority stated that their sales increa sed in the past year (77%). It’s excellent news, especially when compared with last year’s figure of just 46% of stores having an increase in sales. Moreover, this is the largest proportion of stores saying they’ve had increased sales we’ve seen in this survey’s recent history (see Chart C). True, when asked by what percentage their sales increased, stores reported a smaller increase than last year (6.2% versus 13.1%). But nonetheless, it’s encouraging that independent stores are building back what was lost during the down economy.

sed in the past year (77%). It’s excellent news, especially when compared with last year’s figure of just 46% of stores having an increase in sales. Moreover, this is the largest proportion of stores saying they’ve had increased sales we’ve seen in this survey’s recent history (see Chart C). True, when asked by what percentage their sales increased, stores reported a smaller increase than last year (6.2% versus 13.1%). But nonetheless, it’s encouraging that independent stores are building back what was lost during the down economy.

While fewer stores recorded declines than in past years, the amount by which sales fell was more than before (a 19.3% decline). This is somewhat of a trend, as the percentage by which stores with lost sales have fallen has been on a downward slope since 2008, according to WholeFoods data. In 2011, the smaller group of larger decliners certainly impacted the overall decline in revenue to $1,010,644. It’s possible that in the natural evolution of any industry (including ours), only the fittest will survive when times are tough. Stores that have always been marginally profitable and are now consistently seeing declining sales may need to do some major strategizing and restructuring if they want to survive.

Despite the decline in overall sales, it’s a different story when you consider net profit. By net profit, we mean free cash flow available after all expenses, but before taxes. This year, we saw net profits rise to $88,680. Last year, net profits only averaged about $68,322. That’s a 30% increase in profits, which is certainly a good sign of the industry’s health.

health.

We can also put stores of all sizes on equal footing and consider the net profits by square foot. This analysis brings us more good news. This year, net profits by GLA soared to $30.34/ft2,, which is 34% more than last year’s figure of $22.68/ft2. Clearly these are efficient spaces, which lines up with the smaller GLA of this year’s sample. Stores’ average net profit percentage also jumped from 6% to 9%. That’s a 50% leap!

Perhaps the increase in net profit can be partly attributed to smart management, which includes stores doing everything they can to appeal to shoppers with the right products, clever promotions and well thought out advertising campaigns. Let’s take a closer look at the participants’ sales distribution by product category.

Perishables and profits. Over the past few years, WholeFoods has suggested that stores with more sales from perishable foods (including refrigerated/frozen foods, fresh produce, prepared food and the like) tend to have more selling space, greater foot traffic and bigger sales.

The 2011 data again bolster this observation, but there’s a qualifying statement. If not properly managed, having bigger produce- and prepared foods-heavy stores doesn’t necessarily equate to bigger profits. Managing these sections indeed takes talent. Balancing  the expirations with offering a good product mix and just the right quantities of each certainly cannot be left to luck if one wants to be profitable. For this reason, stores should think long and hard before attempting to have a store with a large proportion of these foods. But at the same time, offering too little, as we will see, can be a problem, too.

the expirations with offering a good product mix and just the right quantities of each certainly cannot be left to luck if one wants to be profitable. For this reason, stores should think long and hard before attempting to have a store with a large proportion of these foods. But at the same time, offering too little, as we will see, can be a problem, too.

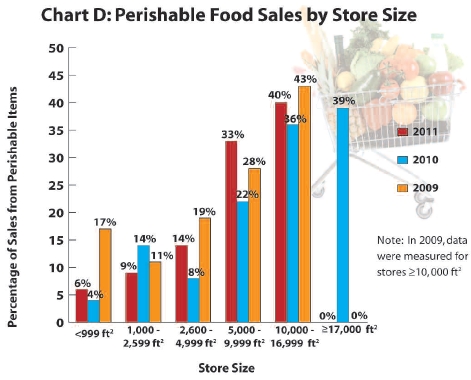

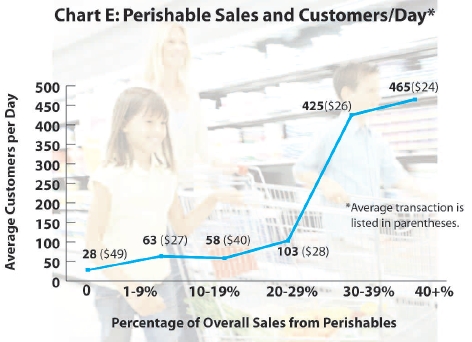

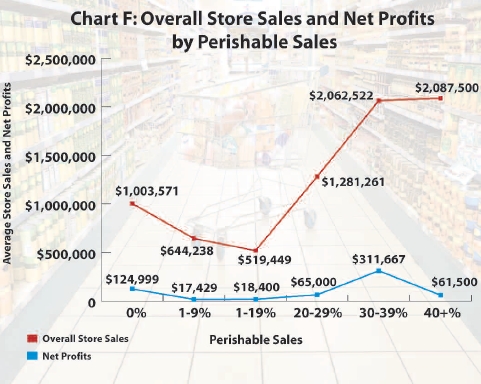

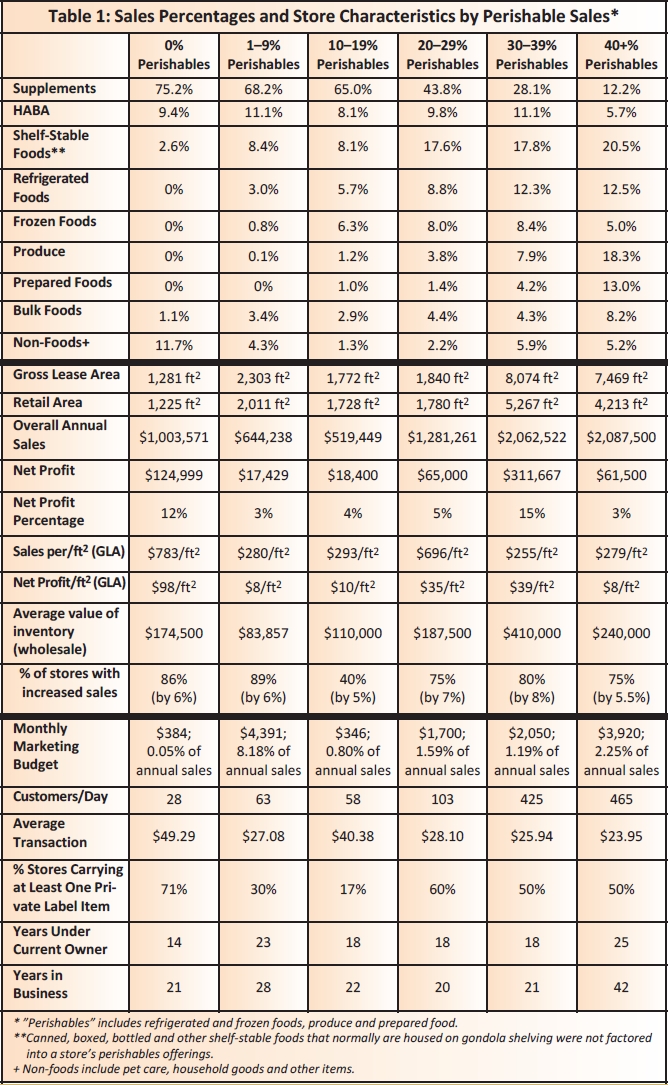

As in past years, 2011’s larger stores also had more perishable sales (see Chart D) and more customers per day (see Chart E), in general. Interestingly, when broken down by percentage of perishable sales, stores with no perishables (0%) offerings at all blew many other stores out of the water with their net profits (see Chart F). Their annual net profits averaged $124,999; the only other group with more profit sold 30-39% perishable foods and made $311,667 in profit. The non-perishables group also had an impressive net profit percentage of 12%. The only higher group, again 30-39% perishables, had a net profit percentage of 15% (see Chart F).

Our non-perishables stores outshone establishments in other revenue figures, too. These businesses also had the smallest footprints, with a GLA of 1,281 ft2 and an average retail space of 1,225 ft2. Their sales and profits by square footage (GLA) were sky high: $783/ft2 and $98/ft2, respectively. Not surprisingly, these establishments were the most supplement-heavy shops with 75% of total sales coming from this department (see Table 1).

This subset of stores teaches us that one need not “go big or go home” necessarily. Small, vitamin-focused retailers have a major role to p lay in our industry. They have a higher staff-to-shopper ratio than the average store, so they are clearly focused on education and customer service. Their shoppers must be listening and dedicated, because they are spending more per transaction here than what we see at other stores ($49.29 per transaction for 0% perishable stores versus $32.02 for all establishments).

lay in our industry. They have a higher staff-to-shopper ratio than the average store, so they are clearly focused on education and customer service. Their shoppers must be listening and dedicated, because they are spending more per transaction here than what we see at other stores ($49.29 per transaction for 0% perishable stores versus $32.02 for all establishments).

Now, let’s look at all stores that sell at least some perishables.

Food, glorious food. Market reports tell us that organic dairy and produce are gateway categories for the natural products industry. Being free of chemicals and growth hormones, these foods get curious shoppers to try and buy. It isn’t long before these shoppers gradually broaden out to buy goods in other categories, too. Maybe a prepared entrée one week or some vitamin C the next.

So it’s really no shocker that the stores with the most sales and net profits were also the ones that sold the most refrigerated items (like milk and cheese), produce, prepared foods and frozen items. Stores with 1–9% of sales from perishable foods relied heavily on refrigerated items and generated little to no sales from areas like prepared foods.

Perhaps having just a few offerings in the refrigerator case was not enough variety to make shoppers visit these businesses for their weekly grocery stock-up or a quick, easy meal (see Table 1). The perception may well be that they are a vitamin shop with some personal care—oh, and by the way, you can grab a carton of eggs here, too, during your vitamin trip.

The 10–19% perishables group may be suffering from a similar problem; with practically no produce or prepared items, their food choices primarily only appeal to shoppers looking for boxes, cans and bottles. One could assume that most natural and organic shoppers are serious fruits and vegetables shoppers who would be forced to shop at another store, too, to fill this need. It’s possible that these buyers don’t always have the time to stop twice and may sometimes decide to shop where the produce offerings are best.

On the positive side, there was a noticeable jump in profits, sales and customer count at the 20% perishables mark. Once stores were at or about this threshold, we saw far greater sales and profits. The 20–29% perishables group is interesting because they had a smaller footprint than the larger perishables stores, so their revenues and profits by the square foot were great ($697/ft2 and $35/ft2, respectively). At this point, it’s likely that customers perceived these stores as places to shop for groceries and also supplements. They meet the need of the busy family that shops weekly for food or that wants a quick, prepared meal for that night’s dinner.

To make sense of the low net profit percentage for the 40+% perishables group in comparison to the profitable 30–39% group, we can again say it takes talent and effort to make large produce and prepared foods sections work well. The 30–39% group, our most profitable at $311,667 per year, has found the perfect balance of supplements and perishables (and produce/prepared foods within that).

The Goldilocks product mix. So, let’s recap. Perishable foods comprise a critical area of one’s store; having too many offerings without the right expertise to manage it all can be catastrophic. At the same time, many stores need enough perishable offerings to get ample foot traffic—especially for the “What’s for dinner?” crowd.

Our middle group of higher perishables sales stores (30–39%) has hit a sweet spot; they’re likely getting a draw from their perishables sales, but this section is controllable. Prepared and fresh produce departments are big, but not so big that the offerings are unmanageable. It’s just right.

A word on the stores with the largest perishables offerings. While some may be going overboard with their offerings, it should be noted that it takes time to refine the heavy perishables approach. Take Whole Foods Market, for instance. They had about 69% perishables sales in the fiscal year ending in September 2010. They’ve had 30 years to fine-tune their approach. While this year’s largest perishable stores may not be the most profitable, perhaps future surveys will see a change as this group develops its expertise.

Clearly, people want to get their nutrition from food and want their food experiences to be fun and fresh. Thus, there’s some pressure on natural products stores to deliver by adding more perishable foods to the product mix. But, attempting to move too far in that direction can be as much of a challenge as tentatively dipping a toe in the water.

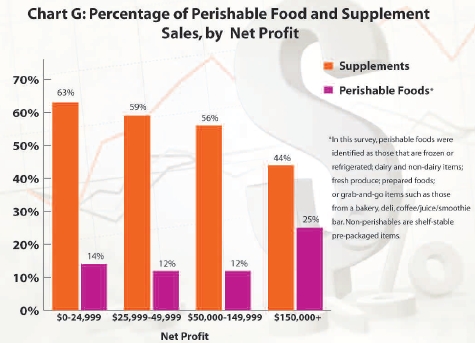

Supplements chic. When the 2011 profits are analyzed by supplement sales, we see an interesting trend. Net profits tend to rise as supplement sales fall and perishables i ncrease (see Chart G). The most profitable stores struck a powerful balance with “critical mass” in both supplements and perishables (see Chart F2). Stores with $150,000+ in net profits had 44% of their sales from supplements and 25% from perishable foods. But, if we divide stores by their supplement sales and look at their net profits, we can identify a small group of profitable, but heavy supplement sellers. These stores—with 90%+ of sales from supplements—are an exception to the rule; they had practically no grocery sales at all (0.8%) but nice net profits of $86,666.

ncrease (see Chart G). The most profitable stores struck a powerful balance with “critical mass” in both supplements and perishables (see Chart F2). Stores with $150,000+ in net profits had 44% of their sales from supplements and 25% from perishable foods. But, if we divide stores by their supplement sales and look at their net profits, we can identify a small group of profitable, but heavy supplement sellers. These stores—with 90%+ of sales from supplements—are an exception to the rule; they had practically no grocery sales at all (0.8%) but nice net profits of $86,666.

While this store type may not work for everyone, it bolsters the idea that shoppers in this industry have diverse needs. But stores need to be assertive about establishing their own identity and underscoring it in their offerings and services. Injecting some foods into a primarily pill shop may make you feel more well-rounded. But, if you want to be the must-stop grocery store for families in your community, consider whether your refrigerated, produce and prepared foods are enough to satisfy the needs of a week’s worth of shopping or putting together dinner in a hurry. If your specialty is selling supplements, you could very well meet your customers’ needs for a knowledgeable vitamin shop with little to no food options. But, setting up camp in a no-man’s land of some—but not enough—perishable foods may not make you as profitable as you can be.

Private Eye

Private Eye

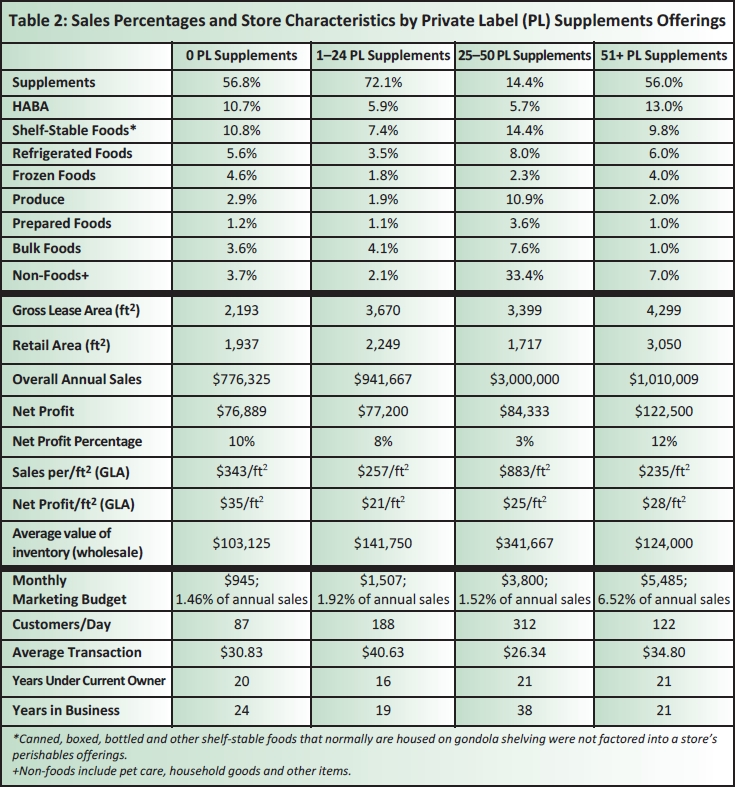

We know that offering private label products is an important way to distinguish your store from the others and to encourage repeat sales. Are private label offerings helping the bottom lines of this year’s survey participants?

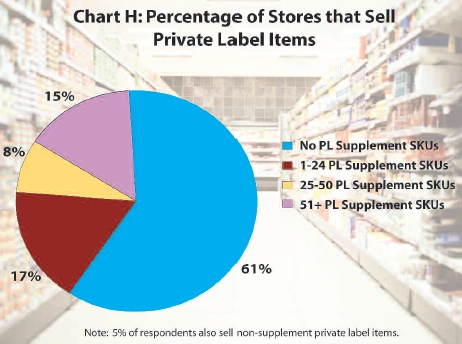

We can start off by noting that 39% of participants sold at least one private label item (see Chart H). That’s slightly more than last year, which recorded 37% of participants selling private label.

This year, we can note a linear correlation between profits and private label offerings. The main trend is that stores that sell private label generally have more sales and net profits than those that don’t (see Table 2).

The net profit percentages for stores also had a fairly linear correlation, though there was a dip in the 25–50 private label supplements group.

As for foot traffic, stores with no private label offerings at all also had the fewest customers per day (87 people). Stores with just 1–24 private label supplements had more than double this amount, with 188  shoppers daily. Carrying just 1–24 private label supplements also made for larger transactions than the non-private label group ($40.63 versus $30.83). It should be noted, however, that while foot traffic and average transaction were greater for the 1–24 private label supplements group, their profits were about the same as the group that sold no private label at all. Again, perhaps we can attribute this to higher expenditures such as payroll ($322,028 annually or 28% of their annual sales versus $119,816 annually or 12% of their annual sales).

shoppers daily. Carrying just 1–24 private label supplements also made for larger transactions than the non-private label group ($40.63 versus $30.83). It should be noted, however, that while foot traffic and average transaction were greater for the 1–24 private label supplements group, their profits were about the same as the group that sold no private label at all. Again, perhaps we can attribute this to higher expenditures such as payroll ($322,028 annually or 28% of their annual sales versus $119,816 annually or 12% of their annual sales).

The group that seemed to fare the best in terms of profit were the stores that had 51+ private label offerings. Their net profit was significantly higher than the others ($122,500, a net profit percentage of 12%), though they had smaller overall sales ($1,010,009) than other stores. These 51+ private label supplements stores must be owned by savvy managers that probably bargain for the best prices from their distributors and sell at just the right price points to maximize profits. It’s likely that private labeling plays a major part in this equation.

Ring ‘em Up!

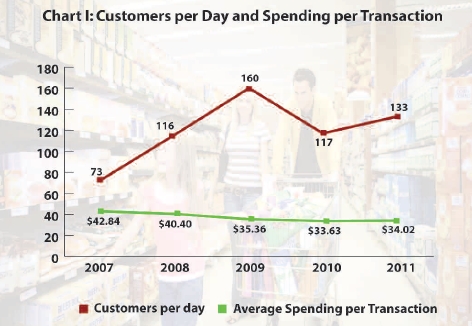

Overall, the number of customers that stores saw each day and the average transaction amount was better this year than what we saw in 2010 (see Chart I). Stores saw about 14% more customers this year than last (133 in 2011 versus 117 in 2010), and the average transaction rose slightly from $33.63 to $34.02. This could be a sign of a slow economic recovery. Let’s look at the characteristics by customers per day to see what we can learn from shops with the heaviest foot traffic.

First, stores with more than 200 customers each day tended to have the largest footprints (4,039 ft2 of retail space). About one-quarter of their overall sales came from supplements, which was the smallest amount of all groups. They also sold the most perishables of all (34.3%), but had the smallest spending per transaction ($26.84). Regardless, foot traffic was such that they also had the most net profit ($189,667, with a net profit percentage of 8%).

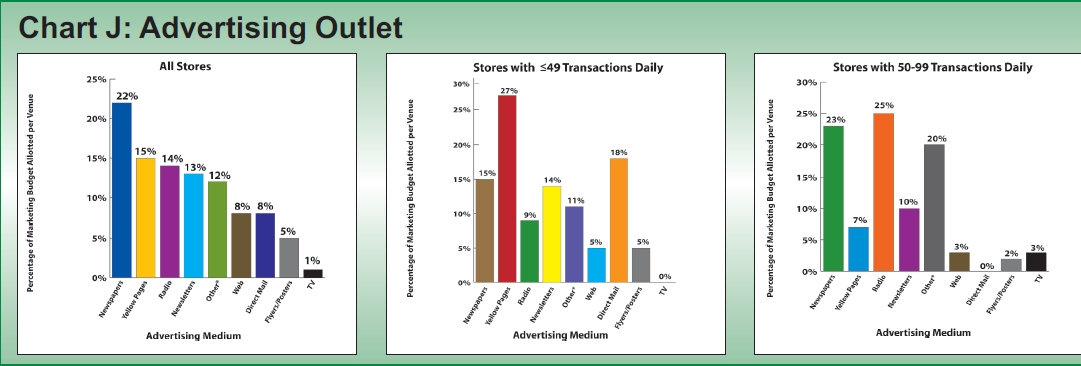

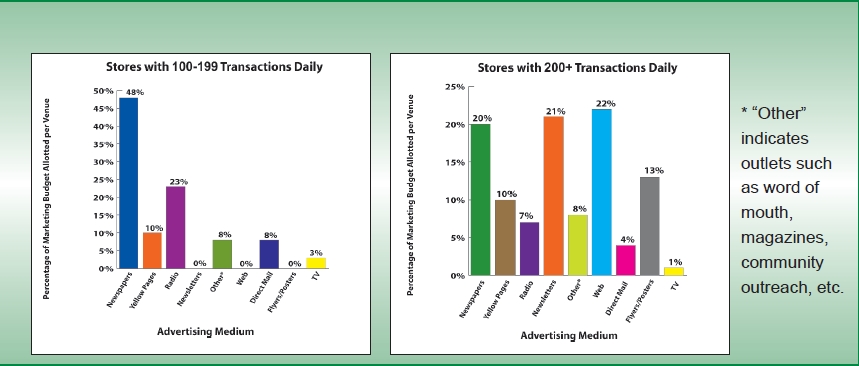

And, stores with the most customers spent slightly more on advertising than other shops ($6,066.70/month or 3% of their annual sales). Their choices for spending this money were interesting, too. Most of this budget went to three major outlets: Web sites (22%), newsletters (21%) and newspapers (20%) (see Chart J1–5). Perhaps their money went a little further, as some of the most expensive advertising venues were not favored by this group (e.g., radio, television and direct mail). Contrast this with the marketing choices of businesses with the least foot traffic (less than 49 people per day). They preferred Yellow Pages, direct mail and newspapers.

Once shoppers were reeled into these stores, the owners used other cost-effective strategies as their top promotional techniques. These included displays and educational handouts. Contrast that with stores with the least traffic. They relied more heavily on samples, coupons and discounts. The latter group ended up with the least net profit ($29,750). While coupons and discounts may seem like economical promotions, one must be careful not to let the discount come out of their store’s bank account. Negotiating for more promotional dollars from suppliers is a better route to profitability.

Once shoppers were reeled into these stores, the owners used other cost-effective strategies as their top promotional techniques. These included displays and educational handouts. Contrast that with stores with the least traffic. They relied more heavily on samples, coupons and discounts. The latter group ended up with the least net profit ($29,750). While coupons and discounts may seem like economical promotions, one must be careful not to let the discount come out of their store’s bank account. Negotiating for more promotional dollars from suppliers is a better route to profitability.

The advertising and marketing choices of stores may offer some additional insight in a store’s “personality,” if you will. Those that see themselves as educators first—and have the confidence to market themselves as nutritional authorities—may prefer outlets like hosting their own radio show or presenting their own informational newsletter. These extroverted stores want to answer customers’ questions head on and help build a nutritional program.

Stores that allotted at least 20% of their marketing budgets to newsletters, for instance, had strong net profits of $176,000, with a net profit percentage of 18%! Those with at least 20% of their marketing budgets earmarked for radio had high net profits of $116,857, with a net profit percentage of 12%.

Remember our 90%+ supplement sales group, with net profits of $86,666 and net profit percentages of 12%? The overwhelming majority chose to establish themselves as nutrition gurus on the radio: 55%! Stores that favored more static and less direct means of interacting with clients (like discounting) had a net profit percentage of 8%.

This may tell us reactive owners who wait for customers to come to them, and don’t establish themselves as nutritional authorities may be losing profitability. Conversely, proud, confident businesses that can prove to customers they have the expertise and right product mix to meet their needs will surely be pillars in their communities for years to come. Bottom line: if you are knowledgeable about nutrition and healthy living, leverage it! WF

Published in WholeFoods Magazine, December 2011